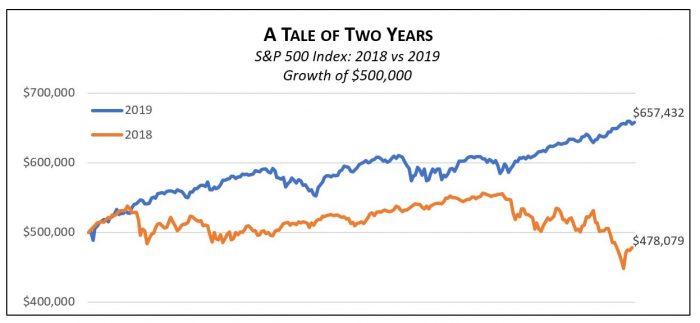

A year ago, markets entered 2019 on high alert amid signs of economic slowing and fears of imminent recession. Following a near bear market at the end of 2018, it seemed as though that old Bette Davis line from All About Eve might apply: “Fasten your seatbelts, it’s going to be a bumpy night.” Instead, the 50th anniversary of Apollo 11 was a more apt metaphor for the 2019 stock market: “Houston, we have liftoff.”

Indeed, the US stock market (S&P 500) rocketed over 9% in the fourth quarter and finished the year with a 31.5% total return, its best since 2013 and second best in the last 20 years. The big jump marked a huge rebound from 2018, when stocks and almost all asset classes fell.

Like every year, we enter 2020 with a new set of trepidations—escalating tensions in the Middle East; a presidential impeachment trial pending; presidential and other elections in November, with a very wide range of political viewpoints represented; and many parts of Australia on fire, a sobering reminder of the reality of climate change. But 2019 reminds us that none of these worries serve as reliable forecasters of the stock market’s coming performance.

Markets Are Like a Box of Chocolates[1]

Two primary factors explain last year’s stock market strength. First, the economy proved more resilient than many expected. Second, interest rates dropped, helped by three Fed rate cuts and a general perception that economic growth, while still positive, is decelerating. That’s the best of both worlds for stocks. You can think of stock prices as a quotient—the numerator is economic strength (corporate earnings) and the denominator is the interest rate. In 2019, the numerator went up, the denominator went down, and the result was a booming stock market. Falling rates were a boon for bonds, too. The leading US bond index boasted a strong 8.7% total return, as declining interest rates pushed up the price of existing bonds.

In heady times like these, we think it’s important to temper expectations. In particular, it is unlikely that the positive impact of lower interest rates on stock and bond prices can continue indefinitely. If one thinks of future securities returns over, say, the next five years, it’s a bit like a 5-pound box of See’s chocolates. Under reasonable projections, you might partition the box into five equal sections and eat a pound a year for five years.[2] But 2019 was as if someone sharply tilted the box, causing most of the chocolates to slide into the first year’s partition. Lower interest rates had the effect of accelerating future returns into the present. This is ok news for investors with already large portfolios, as it simply redistributes returns over time, but it’s more challenging for younger investors trying to build those portfolios and potentially facing lower rates of return on capital invested down the road.

Of course, the economy and corporate earnings could exceed expectations, in which case stocks might continue their tear. But as a general matter, we think investors would be wise to view 2019 as an outlier, with more modest and sustainable rates of return likely ahead.

New Retirement Law (SECURE Act) Changes IRA Rules for Many

In December, the SECURE Act became law, representing the first significant change to retirement plan rules in many years. For our clients, the two most noteworthy changes are:

- Age 72 is New Start Date for Required Minimum Distributions (RMDs). Previously, investors were generally required to begin distributions from IRAs, 401(k), and 403(b) plans in the year in which they turned 70-1/2. This will enable those who can wait to enjoy an extra year or two of tax deferral in their retirement plans. The rule applies to those who had not reached age 70-1/2 by the end of 2019.

- Inherited IRAs Must Be Fully Distributed to Heirs Within 10 Years. Previously, persons inheriting IRAs could stretch distributions over their own life expectancies, greatly extending the IRA’s tax-deferral benefits. With a few exceptions (including spouses), this is no longer the case.

401(k) and 403(b) Contribution Limits Rise in 2020

Effective in 2020, the annual contribution limits for 401(k) and 403(b) plans have been increased to $19,500 (from $19,000) to reflect inflation. Plan participants aged 50 and above can contribute an extra $6,500 (up from $6,000). SEP IRAs and Individual (or Solo) 401(k) plan contribution limits also increase to $57,000 (from $56,000). We’re happy to help review your options.

Schwab Acquires TD Ameritrade

In November, broker/custodian Charles Schwab announced its $26 billion acquisition of TD Ameritrade. The deal followed quickly on the heels of both firms’ elimination of most brokerage commissions. That move pressured both to seek further economies of scale, hence, the combination.

As a result, current customers of TD Ameritrade will ultimately become customers of Schwab unless they choose to move their assets to another custodian. We have more than 10 years’ experience working with clients holding their assets at the two firms, so we foresee no issues with respect to clients with accounts currently at TD Ameritrade.

While the acquisition is slated to close in the second half of 2020, it may be 2022 before the operational transition is completed. In the meantime, we will monitor the transition closely and, as appropriate, will advise our clients currently at TD Ameritrade on what we believe are the most favorable custody arrangements going forward. Clients using Fidelity will not be affected. Please contact us if you have any questions.

[1] As Forrest Gump might have said.

[2] Apart from the obvious problem of candies going stale, we also know how preposterous the idea is of leaving a box of chocolates uneaten for any meaningful period. Bear with us.