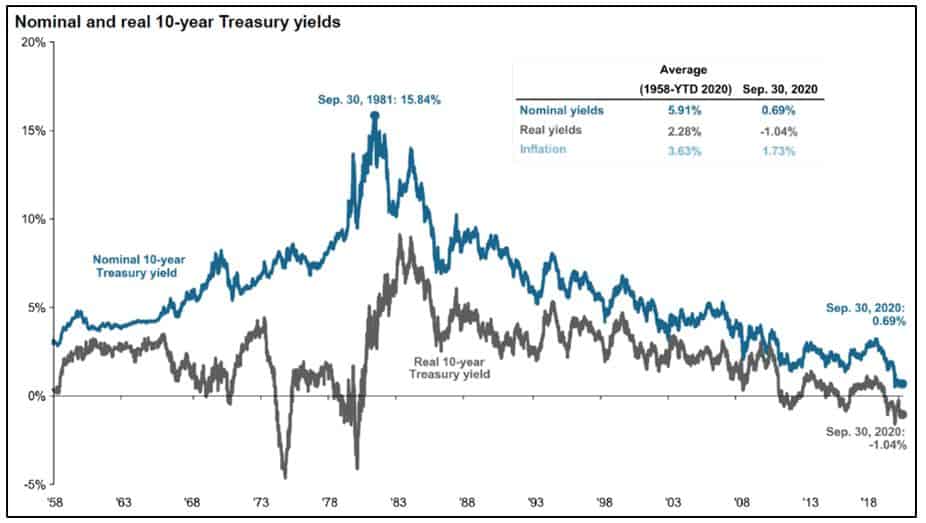

Real Returns

In our recent client webinar[1], company president and chief investment officer Don Gould focused much of his discussion on “real” interest rates; that is, the interest rate after adjusting for the effects of inflation. For example, a bond that pays 3% interest (its “nominal” interest rate) in a 2% inflation environment has a real interest rate of about 1% (3% minus 2%). Since the 1990s, the US Treasury has issued inflation-indexed bonds (known as “TIPS”), enabling investors to explicitly see current real interest rates.

One notable impact of the Covid pandemic and associated economic contraction has been a significant drop in real interest rates. The 10-year TIPS now yields about negative 1%. Yes, you read that correctly. If you buy a 10-year TIP today and hold it to maturity, in 10 years you will have about 90% of the purchasing power of your original investment. Over the past century, US government bonds averaged a return of about 2.5% above inflation, so today’s –1% represents a startling decline.

Why is this so important? Because you can think of the TIPS yield as the foundation of all real return expectations across asset classes. As you take on additional risk—for example, buying corporate bonds or stocks—you add a “risk premium” to the TIPS yield to estimate your expected return on the riskier asset. A corporate bond might carry a 1% return premium over TIPS, while US stocks historically have delivered about a 5% premium.

Assuming that same 5% premium holds going forward, the –1% TIPS yield implies an expected real return on stocks of about 4% (–1% plus 5%). Add 2% for inflation and you’re looking at a 6% annual nominal expected return on stocks, or well below their historical average of about 10%. That means someone today hoping for a 7% portfolio return going forward might not achieve that, even with a 100% stock portfolio.

When the Tail Wags the Dog

We had an occasion earlier this month to join a video seminar sponsored by a large investment consulting firm that advises endowments and foundations. The keynote talk was an interview with a very prominent investor. In the Q&A, the first question posed hit the nail on the head. It was this: considering today’s historically low expected returns on stocks and bonds, how does an investor achieve their long-term rate of return target?

The answer was astounding...astoundingly bad, that is. The celebrated investor advised the audience to ramp up the risk of their portfolios to compensate for lower expected returns on stocks and bonds. This is a little like saying that if the freeway slows, you should start weaving in and out of lanes to maintain your previous speed. Probably you should just slow down with the traffic.

Pushing risk beyond one’s tolerance is invariably a bad idea. When the added risk rears its head—and it always does, eventually—the investor will realize he or she is in too deep and then ratchet back risk, selling riskier assets in exchange for cash and bonds, often at the worst possible moment from a market timing perspective.

A much better answer would have been to counsel the endowments and foundations to lower their expectations, reduce their annual spending rate, tighten their budgetary belts, and perhaps try to generate more donations.

Likewise, for the individual investor, the advice must be to adjust expectations to match market realities. In some cases, that might mean the investor needs to push out a planned retirement date by a couple years, reduce spending for some period, or some combination of the two. Granted, it’s not a cheerful prescription, but it’s the right one.

The Economy and the Election

Recent economic data suggests that the economy’s recovery—the snapback from the plunge in the first lockdown period—is slowing. The pandemic’s impact on consumer behavior has led to large and lasting employment declines in the leisure, hospitality, and transportation sectors, among others. The online economy has largely rebounded to pre-pandemic levels, while the in-person economy struggles, a divergence that has come to be known as the K-shaped recovery—some parts back up, others still down. Efforts to pass another stimulus bill have stalled, and with the election less than three weeks off, it is unclear if or when a bill will be enacted or what it might contain.

The election itself is a source of consternation. Concerns have been voiced over voter suppression, fraudulent ballots, and potentially lengthy counts and recounts. These raise the prospect of protracted post-election battles both in and out of court, and even a Constitutional crisis. Our view is that markets will adapt to either candidate’s victory, but a period of political instability could easily be accompanied by heightened market volatility. We will be monitoring the situation closely and communicating with you, as necessary. To the extent the presidential and Congressional election outcomes lead us to expect meaningful tax law changes after 2020, we will also let you know if we think that necessitates any investment actions before year-end.

Regardless of how events play out, as always, we would counsel you to remain calm and keep in mind that your investment time horizon is much longer than either this election cycle or even the presidential cycle.

[1]https://gouldasset.com/2020/09/mid-september-webinar-and-qa-with-don-gould/