A Sprinting Market…Gasping for Breadth?

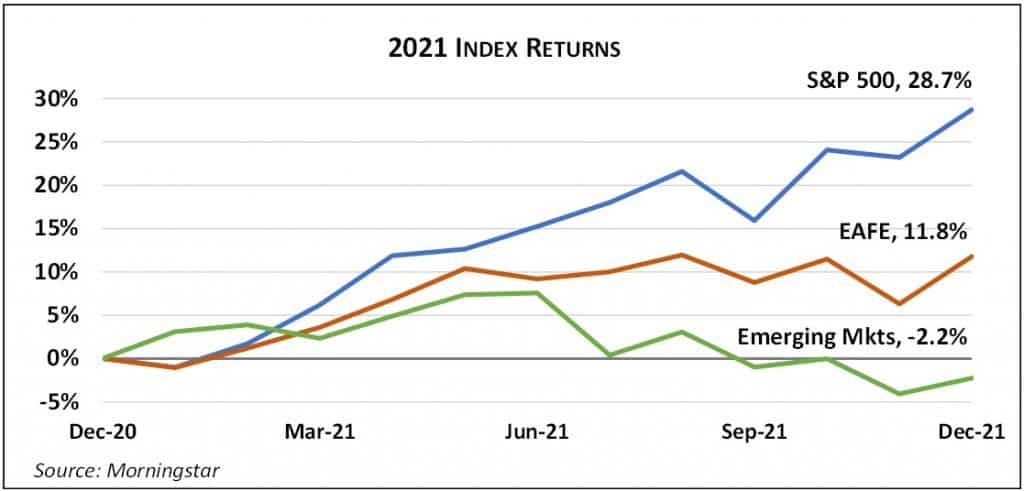

The US stock market rocketed upward by more than 10% in the fourth quarter, finishing another remarkable year at all-time highs. The large cap S&P 500 index returned a whopping 28.7% in 2021. Strong corporate earnings combined with historically low interest rates continued to support stock prices.

2021 marked the third straight year of outsized returns for US large cap stocks, a period in which the index achieved a compound annual return of 26.1%. To put that astounding number in perspective, in the 20 years ended 12/31/21 (a period obviously including the most recent three strong years), the S&P 500 had a compound average annual return of about 9.5%, a reminder that the recent streak is far from the norm.

The booming US indexes mask some cautionary signs. A shrinking number of large growth stocks accounted for most of the market’s gains late in the year, indicating less “breadth” to the rally. The accompanying chart illustrates how a concentrated group of stocks (which included Microsoft, Nvidia, Apple, Alphabet (Google), and Tesla) powered the S&P 500 higher in recent months.

Foreign stock markets also substantially trailed the US last year, meaning breadth was also lacking globally.

A Less Accommodating Fed

We also note last year’s rebound in interest rates off the early pandemic lows and the concomitant decline in bond prices. Steadily declining interest rates have long supported equities by making stocks more attractive in comparison to bonds. With the Fed now curtailing bond purchases and likely soon raising short-term interest rates to try to tamp down resurgent inflation, stock markets face a headwind this year. 2022 has already seen meaningfully higher rates across the yield curve, accompanied by heightened stock market volatility, so we’ll see if stocks are up to the challenge.

We continue to closely watch the course of interest rates because of both their potential impact on stock prices and the effect they may have on economic growth.

Controlling Risk

A rising market tide tends to lift all boats and the converse also applies. Tempting as it may be to try to time the market, no one does it well. Taxes and opportunity cost—being out of the market when it turns north again—make timing a losing proposition.

We manage the risk of downturns through prudent diversification, holding both stocks and bonds, as well as other asset types, in proportions consistent with each client’s tolerance for risk. Diversification within asset classes is important, too; that is, owning both growth and value stocks, domestic and international stocks, and so on. Regular portfolio rebalancing—paring back the biggest winners and reallocating to the lagging sectors—protects against both excessive optimism and undue pessimism while keeping overall portfolio risk steadier through time.

Whither Withering Inflation?

Possibly the biggest question entering 2022 is what course inflation takes this year. Fueled by record amounts of government stimulus, consumer demand snapped back from its pandemic lows much more quickly than businesses could crank up supply. When demand grows faster than supply, prices rise, aka inflation. US inflation surged last year to over 7%, a level not seen in 40 years.

Sustained higher inflation is particularly damaging to long-term fixed-rate bonds, as it reduces the purchasing power of future interest and principal payments. The relatively modest decline in bond prices last year reflects a market consensus that the pandemic will recede, supply will adjust upward, and inflation will fade to something closer to the 2% level that has prevailed since the mid-1990s. The Fed seems determined not to let expectations of higher inflation become ingrained, even at the cost of higher interest rates that could slow the economy and drive market turbulence in the coming months.