Crystal Balls are Overrated

This first quarter of 2024 marks the four-year anniversary of the beginning of the Covid pandemic. Yes, hard to believe, but it’s really been four years since an invisible virus upended our world. Together, the pandemic’s onset and the subsequent performance of financial markets reinforce two points we preach daily.

First, the future is unknowable. On New Year’s Day 2020, hundreds of thousands thronged to the Rose Parade in Pasadena, and probably none could imagine a world in lockdown less than three months later.

Second, even if one could foretell the future like some Greek oracle, the markets’ response to that future will repeatedly confound you. We include in every quarterly report a chart that superimposes the period’s news headlines over a graph of stock market performance. The not-too-subtle message is that there’s usually not much connection between the headlines and the markets.

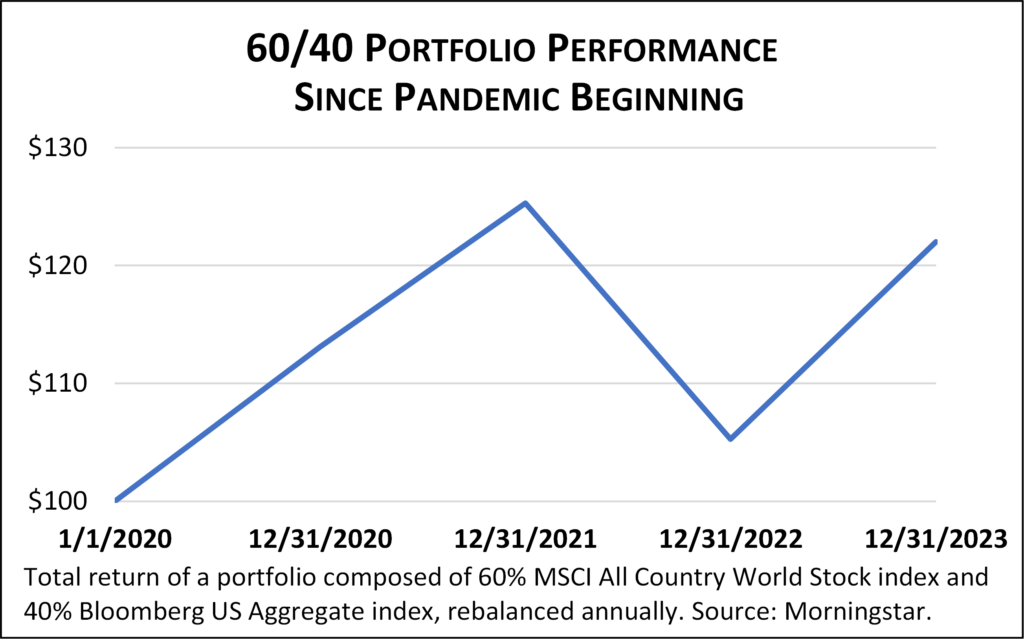

Returning to our case in point, if your crystal ball had told you that in the US alone the pandemic would cause an immediate loss of 25 million jobs, more than one million deaths, and stretch out 2-3 years, you probably would not have predicted very strong stock markets in three of the last four years or the highest inflation in decades. Yet, that’s what happened. Our Rip Van Winkle investor, who began a 4-year nap on New Year’s Eve in 2019, would have awakened this past New Year’s Eve (blissfully unaware of all the period’s turmoil) to find a balanced portfolio index[1] had compounded at a middle-of-the road 5% annual rate during the nap.

What a Difference a Year Makes

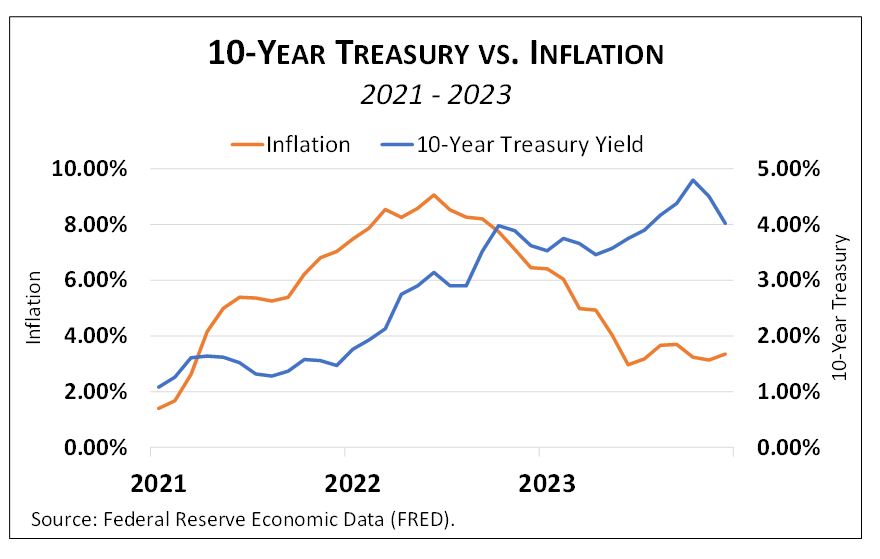

At this time a year ago, financial markets were licking their wounds after a historically bad 2022. Massive early pandemic government stimulus caused inflation to begin accelerating in early 2021. By mid-2021, central banks responded, initiating an 18-month series of interest rate hikes. Together, inflation and higher short-term rates pushed bond yields sharply higher through most of 2021 and 2022. In 2022, the leading US bond index delivered its worst return ever (by a wide margin), losing about 13%. (Remember, rising interest rates push down the price of existing bonds.) Stocks fell even more in 2022, down about 18%. With both main asset classes plunging, balanced portfolios of stocks and bonds turned in one of their poorest years on record in 2022.

Fast forward twelve months and the past year’s picture is radically different and better. With interest rates stabilizing, economies showing resilience and growth, and investors seeing big profit opportunities in artificial intelligence, global stocks rebounded nearly 23% last year, slightly more than erasing all of 2022’s decline. Meanwhile, US bonds were back in the plus column, returning about 5.5%. Inflation continued to subside throughout the year, leading the Federal Reserve to suggest in mid-December that the course of interest rates could soon pivot downward, good news for both stocks and bonds.

Playing the Long Game

While it’s fine to revel in 2023’s year-end statement values, especially after the trauma of 2022, we remind clients to stay focused on their longer investment time horizons. It’s easy to feel as high today as we felt low a year ago, but fear and greed are the long-term investor’s twin nemeses. Huge market swings over the past four years provided numerous opportunities for overreaction and self-inflicted wounds, for example, selling stocks early in the pandemic or after 2022’s historic decline, either of which would have been bad moves. A big part of our job is helping clients navigate these emotional swings, making sure we stay the course we’ve carefully established in calmer times.

2024 surely holds many more surprises in store, both in the news itself and how markets react to those headlines. We’ll do our best to make it a pleasant financial journey for you.

[1] Total return of a portfolio composed of 60% MSCI All Country World Stock index and 40% Bloomberg US Aggregate Bond index, rebalanced annually.

For a fuller discussion, be sure to see our Q4 Economic & Market Review.