We hope this note finds you well.

War Jolts Markets

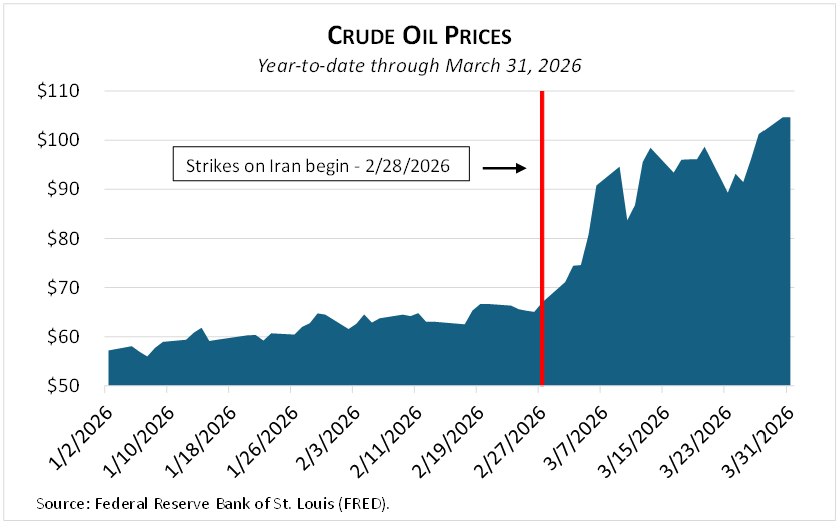

After a modestly positive first two months of the year, markets were jolted by the joint US/Israel surprise airstrikes on Iran at the end of February, triggering a worldwide slide in stock prices that continued through most of March.

Iran’s effective closure of the Strait of Hormuz immediately reduced world oil and gas supplies by roughly 10% and 20%, respectively, causing prices to soar. The net importers of Asia and western Europe saw energy costs spike 50%-150%. Even in the energy-rich US, gasoline prices are up over 30% in just a month. Rising energy costs inevitably mean higher prices for almost all goods.

As we saw during the Covid pandemic, the modern economy depends on highly interdependent global supply chains. When chain links break, unintended consequences follow. Case in point—the Middle East is a major source of fertilizer and helium exports, both curtailed by the war. A lasting fertilizer shortage would mean higher food prices everywhere and potential crop failures, especially in developing countries. Helium is needed for a variety of industrial processes, from making the chips that power AI to the cooling of MRI machines.

As we write this, a tenuous two-week cease-fire is in effect, a first round of negotiations did not result in agreement, and the US has imposed a limited blockade on the Strait of Hormuz. Rumors of further talks are circulating, but the fog of war is dense. The situation is fluid and unpredictable.

Investment Implications

In this conflict, markets must contend with an unusually long list of unknowns. Will the cease-fire hold? Will it lead to a lasting peace or will hostilities soon resume? Will the Strait of Hormuz reopen, how fully, and when? When will this war be over for good? (Prediction market odds on an end by June 30 jumped from 50% to 85% since the cease-fire announcement.) How quickly can energy supplies rebound to pre-war levels, especially considering war damage to oil and gas infrastructure? How might the post-war geopolitical landscape look different? Answers to these questions could determine whether the global economy continues its expansion or falls into recession, so it’s no surprise that markets gyrate with each hint of either resolution or escalation.

Markets and central banks find themselves in the uncomfortable spot of worrying at once about both inflation and recession. Energy supply shocks push up prices—one stark example is a doubling of transcontinental airfares in March alone. But more money spent on airfare leaves less money for everything else. Absent a jump in household income, a sudden rise in the price of something as essential as energy will tend to depress economic activity.

Higher inflation expectations push up bond yields and generally lead to tighter monetary policy (higher short-term interest rates), while recession fears do the opposite. Market yields have reflected this tug-of-war in recent weeks, rising through most of March but easing towards month-end as recession concerns grew. The Fed faces a conundrum.

The war has also pressured the US bond market in other ways. A recent Bloomberg article notes that reduced oil revenue is lessening Middle East oil producing nations’ demand for US Treasurys, while higher oil prices are forcing emerging markets governments to sell Treasurys to cover their higher energy bills. Both actions tend to push yields up and bond prices down.

Yet with all that as a backdrop, in the first half of April, US stocks recovered all their March losses, demonstrating again the market’s ability to confound.

Patience and Perspective are Your Friends

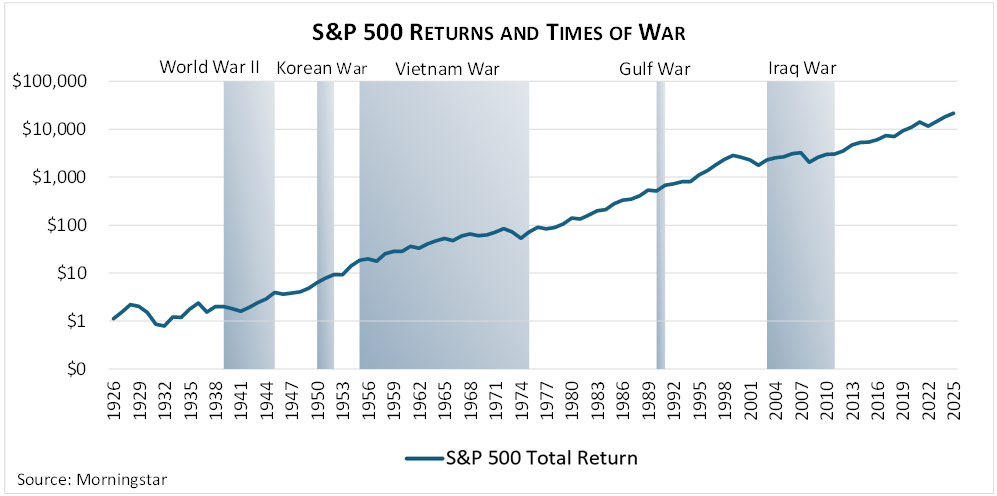

When it feels like the world is spinning so fast that it might come off its axis, we counsel patience and perspective. All wars eventually end, some quickly and some not, some in a lasting resolution and others in stalemate. This conflict is no exception. Short attention spans, as well as political and economic pressures, favor a quicker end, but the jury is still out. The end, when it comes, might be messy and inconclusive. Even a quick resolution will leave world commerce bruised for some period, but history suggests that economies have a natural tendency towards repair, recovery, and resumed growth.

Your advantage amid the discord is that your investment portfolio has a very long attention span. While its market value unavoidably bounces around in response to the nonstop din emanating from the world’s capitals, your portfolio is neither distracted nor diverted from its long-term mission. We aim to keep it that way.

AI Omnipresence

Like you, we watch in amazement as AI finds its way into the nooks and crannies of our work and home lives. We marvel at the capabilities of chatbots like OpenAI ChatGPT, Google Gemini, and Anthropic Claude. Challenged with complex questions, in seconds they spin out well written, thoughtfully organized, apparently deeply researched, highly polished, authoritative sounding answers.

Since the industrial revolution, technology has lessened the need for physical human labor, sending many of us to gyms just to keep our bodies from falling into disrepair. AI is the next step in this evolution, evidently reducing our need to think, as well. Will we all need to rely on Sudoku and Wordle to keep our brains from atrophying?

A cautionary note: remember that the “A” stands for artificial. The intelligence is magnificent, but it is not human. We need to beware the wax museum aspect of all this. That figure of Ronald Reagan at Madame Tussaud’s in Las Vegas looks so lifelike that we feel the Gipper might speak at any moment. And yet, even if skillfully animated to walk and talk, it’s still not Reagan. Likewise, we need to stay alert to the important difference between human and artificial intelligence.

Our business—helping clients achieve lifetime financial security—is fundamentally a human-to-human interaction between advisor and client. What we do requires intelligence, but also critical thinking, empathy, and always a commitment to putting our clients’ interests first. We keep these in mind as we think about the rapid emergence of artificial intelligence in our professional and personal lives.

PS – The cartoon above, which pokes fun at AI’s limitations, was generated in less than one minute from a prompt we gave to Google Gemini AI.

For a detailed discussion of the economy, financial markets, and investment performance, be sure to see the Q1 Economic and Market Review.

Thank You

As always, we thank you for your business and for the trust you place in us daily. Please call or email whenever we can be of assistance.

The Gould Asset Management Team