by Don Gould

I remember as a 10-year-old the wonder of my first passbook savings account. It was with a savings & loan (S&L), a bank-like company that focused on home mortgages. The savings account paid a 5.25% interest rate.

Every time I visited the S&L to deposit money I had earned from odd jobs, I would hand the teller the cash and my passbook, which resembled a passport. The teller inserted the passbook into an electric typewriter-like machine that printed the date and amount of the deposit, the interest I had earned since my last deposit, and my new balance. The teller would return my passbook and I’d hop on my Schwinn, feeling a little richer. It was all so Jimmy Stewart.

I marveled at how my balance increased by this amount called interest. What had I done to earn this? My parents explained that the S&L took my deposit and lent it to some strangers to buy a home they couldn’t otherwise afford, and everyone was the better for it. Still, it felt more like magic than banking. At 5.25%, I could double my money in under 14 years without so much as lifting a finger.

Thanks to deregulation, in the 1980s S&Ls started using depositors’ money for things much riskier than home loans, like speculative real estate purchases. When many of these investments soured, S&Ls failed in large numbers, necessitating a large federal bailout. In the aftermath, the government decided that S&Ls were unnecessary, so the surviving ones were forced to convert to banks. Thereafter, only banks were permitted to make stupid investments (See: Great Financial Crisis, 2008).

Fast forward to 2021. Passbooks are a museum relic. Money moves electronically, everywhere, all the time. Venmo, PayPal, Apple Pay, ACH, crypto, you name it. Even checks and plastic will soon be obsolete.

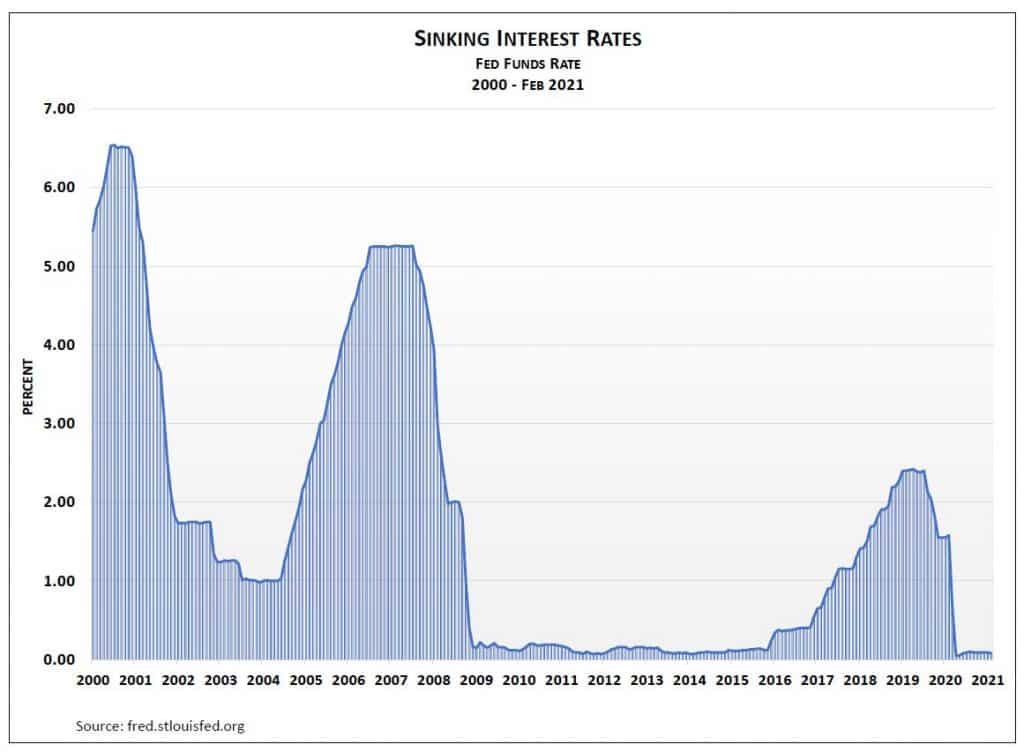

Another thing that’s different today is that banks pay almost no interest. Visit the banks on Yale Avenue in Claremont to discover that the largest US banks all pay 0.01% on savings accounts. Your $10,000 deposit earns you $1 interest per year. After three years, you can use your accumulated interest to buy a cup of coffee. Or you can let your interest compound, in which case your money will double by the year 8953. (I’m not making that up.) Arguably, it’s misleading to call a 0.01% account “interest checking.” Instead of a free toaster when you open a new account (as was once the custom), you should be given a magnifying glass.

And why are interest rates so pitifully low? Policymakers like the Federal Reserve believe that cutting interest rates stimulates economic activity. The theory is that borrowers will: (1) take their interest savings and spend it; (2) borrow more and use the funds to start or expand a business; and/or, (3) spend more because lower rates have pushed up the price of their stocks, bonds, and real estate—the so-called “wealth effect.”

Both the Great Recession of 2008 and the pandemic of 2020 caused sharp economic downturns, leading the Fed to push short-term interest rates towards zero. Money in the bank now behaves like money stashed in a piggy bank or under a mattress—it just sits there, not growing.

Happily, at least a couple workarounds could get you more than 0.01% on your bank savings.

First, if you are okay working with an internet-only bank, consider Ally, Synchrony, or the many others. Most currently pay around 0.50% on savings accounts. Not much, but a lot better than 0.01%.

Don Gould is president and chief investment officer of Gould Asset Management.